House Rent Allowance Calculation for Tax Exemption

House Rent Allowance is a Tax Free Income under Section 10(13A) of the Income-tax Act, subject to the following conditions

House rent allowance [Section 10(13A)] of the Income-tax Act

As per section 10(13A), read with rule 2A of the Income-tax Act, the exemption in respect of HRA will be lower of the following amounts:

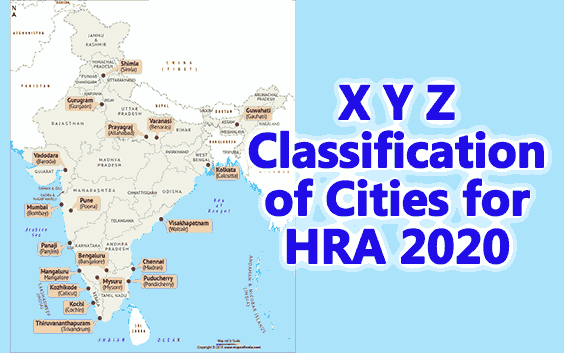

(1) 50% of salary, when residential house is situated at Mumbai, Kolkata, Delhi or Chennai and 40% of salary where residential house is situated at any other place.

(2) HRA actually received by the employee in respect of the period during which rental accommodation is occupied by the employee during the previous year.

(3) Rent paid in excess of 10% of salary.

Salary will include basic salary, dearness allowance forming part of salary while computing all retirement benefits and commission based on fixed percentage of turnover achieved by the employee. Apart from this, salary for this purpose does not include any other allowances/perquisites.

Salary for this purpose shall be computed on due basis in respect of period during which the accommodation is occupied by the employee in the previous year. Hence, any payments not pertaining to the previous year or not pertaining to the period of occupation of the accommodation shall be excluded

[As amended by Finance Act, 2017]